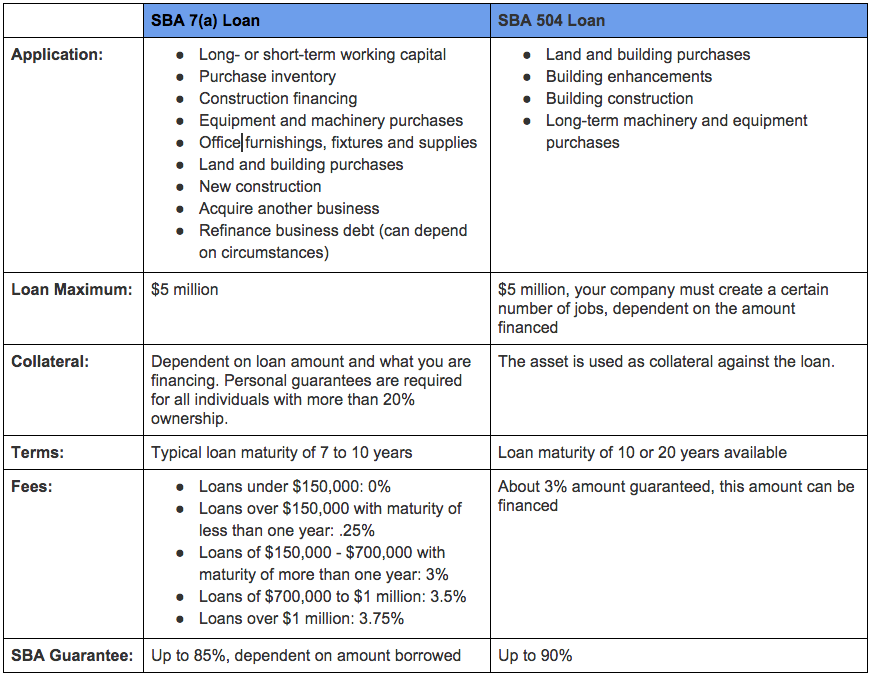

504-7a Loan Comparison

If you’re looking for a small business loan to purchase commercial real estate or heavy machinery/equipment, the SBA 504 loan is the best choice. If purchasing a business or getting working capital is the goal, the SBA 7A loan is likely the better tool.

Read more on expert tips on picking the right loan for your business

More explicitly, with a SBA 504 loan, proceeds can be used to buy a building, finance ground-up construction or building improvements, or purchase heavy machinery and equipment. 7a loan proceeds can be used for short-term or long-term working capital and to purchase an existing business, refinance existing business debt, or purchase furniture, fixtures and supplies.

SBA 504 loans

These loans were designed by the SBA specifically for owner-occupied real estate or long-term equipment purchases. They are composed of two loans: one from a bank for 50% of the loan, and the other from a Certified Development Company for 40% of the loan. You must put at least 10% down.

Pros:

- Below-market interest rates.

- 10- and 20-year terms.

- Low down payment.

Cons:

- Only available after exhausting alternatives.

- Public policy restrictions on eligibility.

- Slow funding process.

SBA 7(a) loans

Using the SBA’s flagship loan, you can borrow up to $5 million through an affiliated lender, depending on your company’s size. These loans can be used to construct new property, renovate property and purchase land or buildings. Rates are based on the WSJ Prime Rate plus a margin of a few percentage points.

Pros:

- Below-market interest rates.

- 25-year term.

- Most loans are fully amortized.

Cons:

- Limits on company size.

- Requires satisfactory credit score.

- Lengthy approval time.

Hard-money lenders

Hard money loans are short-term loans based on the value of the property. These loans are usually made by private companies and tend to have higher down payment requirements. Qualifying for the loan is easier and getting the loan tends to be faster than a traditional mortgage.

Pros:

- Doesn’t evaluate borrower’s credit rating.

- Fast approval.

- Easier to qualify for.

Cons:

- Higher interest rates.

- LTV often capped at 70% to 75%.

- Short-term financing.

At-A-Glance Comparison

SBA 504 LOAN(Commercial Real Estate & Equipment)90% Fixed-Rate |

SBA 7(a) LOAN(General Purpose) |

|

|---|---|---|

| LOAN SIZE | Minimum – $125,000 Maximum – $20 million + |

Minimum – $50,000 Maximum – $5 million |

| INTEREST RATE | • Fixed | • Predominantly variable; some fixed-rate options |

| TERMS | • 20 years – real estate • 10 years – equipment |

• Up to 25 years – real estate • Up to 10 years – business acquisition, equipment • 5 to 7 years – working capital • Weighted average for mixed-use requests |

| DOWN PAYMENT | • 10% borrower | • Minimum 10% borrower(often more) |

To check on qualifying for a SBA 504 loan, small business owners can click here to complete our Commercial Real Estate Questionnaire. One of our experienced Loan Experts will contact them within 48 hours.

For more information on a SBA 7A loan, please click here.

Other Comparisons (details for lenders)

SBA 504 LOAN(Commercial Real Estate & Equipment)90% Fixed-Rate |

SBA 7(a) LOAN(General Purpose) |

|

|---|---|---|

| ELIGIBLE BUSINESS SIZE | • Business net worth not to exceed $15 million • Average net profit after taxes for 2 consecutive years not to exceed $5 million |

• Determined by industry type • Annual sales not to exceed range of $750,000 to $33.5 million for retail, service and agriculture • Number of employees not to exceed range of 100 to 1,000 for wholesale and manufacturing |

| LOAN STRUCTURE | • 50% bank loan • 40% CDC loan • 10% borrower down payment |

• Loan structure negotiable; dependent on risk • 10% down payment (minimum) |

| PROCEEDS USE | • Purchase existing building • Land acquisition and ground-up construction (can include soft cost development fees) • Expansion of existing building • Finance building improvements • Purchase equipment |

• Expand, acquire or start a business • Purchase or construct real estate • Refinance existing business debt • Buy equipment • Provide working capital • Construct leasehold improvements • Purchase inventory |

| PROGRAM REQUIREMENTS | • 51% owner occupancy for existing building • 60% owner occupancy for new construction • Equipment must have minimum 10-year economic life |

• 51% owner occupancy for existing building • 60% owner occupancy for new construction • All assets financed must be used to the direct benefit of the business |

| COLLATERAL | • Generally, project assets being financed are used as collateral • Personal guaranties of the principal owners of 20% or more ownership are required |

• Subject assets acquired by loan proceeds • Pledge of personal residence unless bank can justify why unnecessary • Personal guaranties of the principal owners of 20% or more ownership are required |

| FEES | • Fees are financed in the 504 loan • Fees are negotiated for the 50% bank loan • Servicing fee (lowest allowed by SBA) for CDC plus a legal review fee |

• Fees can be financed in the 7a loan • Fees vary with the size of loan paired with 504 loan • Additional .25% charged on any loan portion above $1 million |

Expert tips on picking the right small business loan for you – SBA 504 vs SBA 7a

The onslaught of guidelines for both options can easily overwhelm even the savviest of consumers. But armed with the right knowledge, you’ll be able to confidently choose the better program for your specific needs.

Check out the key differences between each loan type and when they’re best deployed.

What are the key differences between the SBA 504 and 7a?

First, the basics. An SBA 504 loan is commercial real estate financing for owner-occupied properties. These loans require only a 10 percent down payment by the small business owner and funding amounts range $125,000 to $20 million.

On the other hand, SBA 7a loans can be used to buy a business or obtain working capital. The maximum loan amount is $5 million.

A 504 loan’s interest rate is fixed, and no outside collateral is required. Also, fees are lower compared to a 7a loan. Currently, 504 loans are amortized over 20 years, and began to accept applications for the new 25-year term SBA 504 loan, as of April 2018.

The interest rate on a 7a loan, however, can be adjustable and tied to the prime rate. Collateral is required, at 90 percent. These loans are amortized over 25 years.

Here’s some history and more specifics on each program: The SBA 504 loan program was designed for small businesses to finance commercial real estate or large equipment for use in the business operations.

The 7a loan program was originally designed for higher-risk loans for things like the acquisition or starting of a business, working capital, or furniture and fixtures and leasehold improvements.

What’s a common situation where an SBA 504 loan is the better choice?

When there are multiple partners where one has more assets and equity in their home than the other. Again, an SBA 504 loan does not take a lien on any outside collateral or a home whereas a 7A loan does. If a 7a loan is used in this scenario, it becomes unfair to the more asset-rich partner.

Fees on 7a loans tend to rise with the project size. For example, the guarantee fee for a loan over $700,000 is 3.5 percent — for a project up to $1 million. When the project exceeds $1 million, the rate jumps to 3.75 percent.

However with the 504 loan, the fees involved stay flat as a percentage whenever the loan amount increases. On a $1.25 million commercial real estate project, the fees for a 7a loan can top $27,891, while the fees for a 504 loan are just over $13,306.

Also, the down payment required for the $1.25 million 7a loan would be $187,500 while the down payment for the 504 loan would be $125,000. Thus, in this scenario, there’d be a $77,085 out-of-pocket savings to the borrower if the property was financed with a 504 loan.

Why is the 504 vs. 7a question such a common one among prospective borrowers?

Most borrowers go to their bank of account first when looking to finance real estate, so they may only be offered a 7a option. Once they start to do some research, they’ll usually find out about the 504 program.

In what situation would a 7a loan be a better fit?

When a business purchase is being combined with a real estate purchase and there is a need to borrow working capital. All of these can be rolled into one SBA 7A loan. SBA guidelines forbid using 504 loans to finance a business purchase or for working capital.

Can you use a 7a loan to buy commercial real estate?

Yes, this is possible. However, the 7a option would be more expensive as it relates to the SBA guarantee and SBA fees. Also, banks are not supposed to finance those fees with the loan proceeds, so there is a much more expensive up-front cost with 7a loans.

Here’s a hypothetical situation: For projects where the property price combined with tenant improvement exceeds $775,000 — the dollar-cost difference is dramatic. In this case, the fee for the 504 loan would be 1.2 percent of the total loan compared to 2.9 percent for the 7a loan.

What’s more, if the 7a loan is financed at 90 percent LTV (loan to value), there is usually a lien on the home, the business (UCC), or both. SBA 504 loans do not require any liens on personal residences.

Can you clear up any top misconceptions about the SBA 504 program?

Borrowers tend to think 504 loans are more complicated and harder to qualify for compared to 7a loans. Also, they often view the 504 loan prepayment penalty as onerous.

Those are all misconceptions. First, the lending process for a 504 loan is similar to that of a bank loan’s. And it may actually take longer for a 7a applicant to be approved since outside collateral is required by the program. That’s not required from 504 borrowers.

Lastly, the prepayment penalty for 504 loans is actually less expensive than the 7a in fees and the prepayment amount. The exception: when the 504 borrower prepays in a year’s time.

What is the most common question or concern you get from borrowers regarding the 504 loan?

Borrowers are typically concerned that the process will be long and difficult because they will need approval from the bank, the CDC and the SBA.

Rest assured, if you provide a complete financial package, you’ll be able to meet any reasonable deadline these parties may have. And the timing will be no different if you decided to go with a conventional loan or a 7a loan.